-

New AI cameras detect phone use on France-Spain motorway

The pilot project caught thousands of motorists using their phones while driving

-

Aix-en-Provence creates France’s first parking spaces for small, no-licence cars

Orange bays are for vehicles under three metres long and the scheme also includes free electric charging and discounted parking in the city centre

-

When will fuel prices in France drop after oil price fall?

Both petrol and diesel costs increased across July as tensions flared in the Middle East

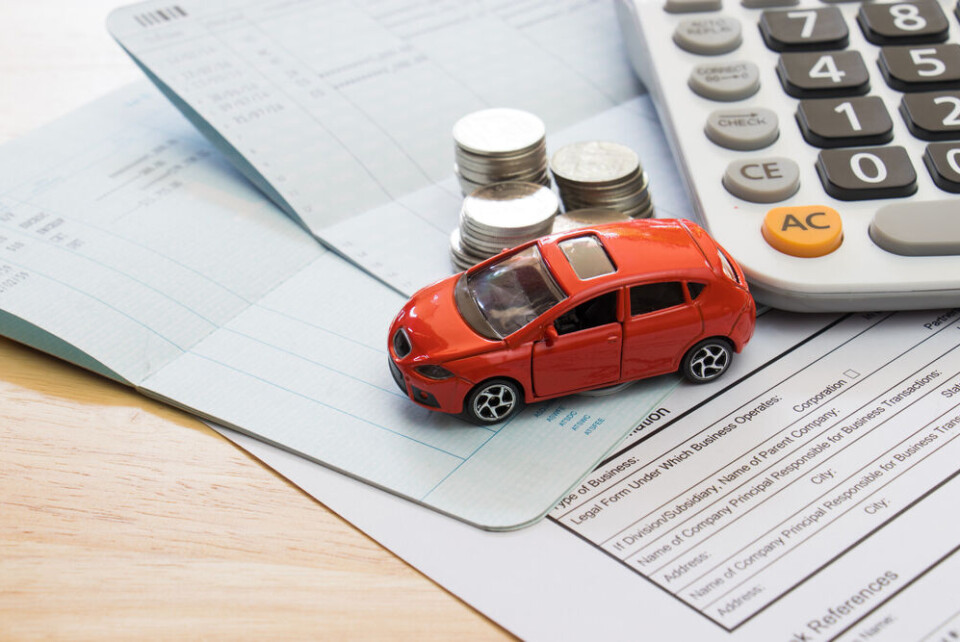

What should you expect to pay for car insurance in France?

Prices continue to rise - and premiums too - industry report shows

Car insurance prices have risen considerably in France over recent years, an industry report by leading online comparison site Lesfurets.com shows, with drivers increasingly comparing offers as premiums continue to increase.

The most recent report (on 2025 data) highlights a sharp rise in comparison activity, with a 23% increase in insurance quote requests in 2025 compared with 2024, reflecting growing pressure on household budgets.

It also points to a broader upward trend in premiums, alongside major shifts in driver behaviour and vehicle choice.

Policy types

In 2025, average costs by policy type were:

- €1,147 for a fully comprehensive policy (+4% vs 2024)

- €671 for third-party cover only (stable vs 2024)

- €942 for third-party cover with additional options such as theft or fire (+1%)

The data shows that while all-risk policies remain dominant, pricing pressures persist across all coverage types.

Location effect: Brittany cheapest

The barometer also shows significant regional variation.

Brittany remains among the cheapest regions, with an average cost of around €798 per year.

In contrast, Provence-Alpes-Côte d’Azur is among the most expensive, at about €1,176. Other costly regions include Île-de-France (€1,082), Auvergne-Rhône-Alpes (€1,005), Hauts-de-France (€939), and Grand Est (€937).

At the extremes:

- Brittany: €798

- Martinique: €1,299

- Mayotte: €472

These differences are mainly explained by claims rates, traffic density, accident frequency, theft levels, and exposure to climatic risks such as storms and flooding.

Type of vehicle

The type of vehicle also plays a major role in pricing, including make, model, age, and engine type.

Interest in electrified vehicles has risen sharply:

- +113% increase in hybrid insurance quote requests in 2025

- +85% increase for electric vehicles

Insurance costs have also risen:

- Hybrid vehicles: €1,178 per year (comprehensive cover, +7%)

- Electric vehicles: €1,125 per year (comprehensive cover, +11%)

This increase is partly linked to the end of the TSCA tax exemption for electric vehicles in 2025, as well as higher repair costs due to more complex technologies and specialist components.

No-claims bonus effect

A driver’s no-claims bonus remains a major factor in determining premiums.

For example:

- A driver with a long claim-free history (CRM 50) pays around €639 per year

- A mid-range driver (CRM 51–90) pays around €953 per year

- A high-risk or young driver profile (CRM 91–100) pays around €1,481 per year

These differences reflect how insurers adjust pricing based on perceived risk.

Age averages

Unsurprisingly, 18–25 year-olds pay the most for car insurance.

In 2025, average premiums were:

- Age 18–25: €1,446 (+1%)

- Age 26–35: €1,012 (+5%)

- Age 36–45: €821 (+6%)

- Age 46–55: €742 (+5%)

- Age 56–65: €672 (+7%)

- Age 66 and over: €677 (+7%)

Premiums generally fall with age, although increases are seen across all groups.

Want to change policy?

Since the introduction of the Hamon law in 2015, policyholders in France can change car insurance provider at any time after the first year of a contract.

The new insurer is required to handle cancellation and the switch.

Cédric Ménager, managing director of Lesfurets, said:

“With insurance rates continuing to rise, now is the time to take stock of your policy and your needs to avoid paying more than necessary.”

He added that comparing offers remains essential, particularly as pricing becomes increasingly segmented by profile, territory, and risk exposure.