-

Finding Your French Home: How an International Buyer’s Agent Is Changing the Game in Toulouse

Lianna Blazquez and her company, International Property Hunter, aim to make finding a property considerably easier

-

Is France heading for a severe drought this summer?

‘This is the first time in 33 years that we’ve had to start releasing water this early in the season’

-

France to merge vacant home taxes from 2027

Two taxes levied on vacant homes to be replaced by a single tax

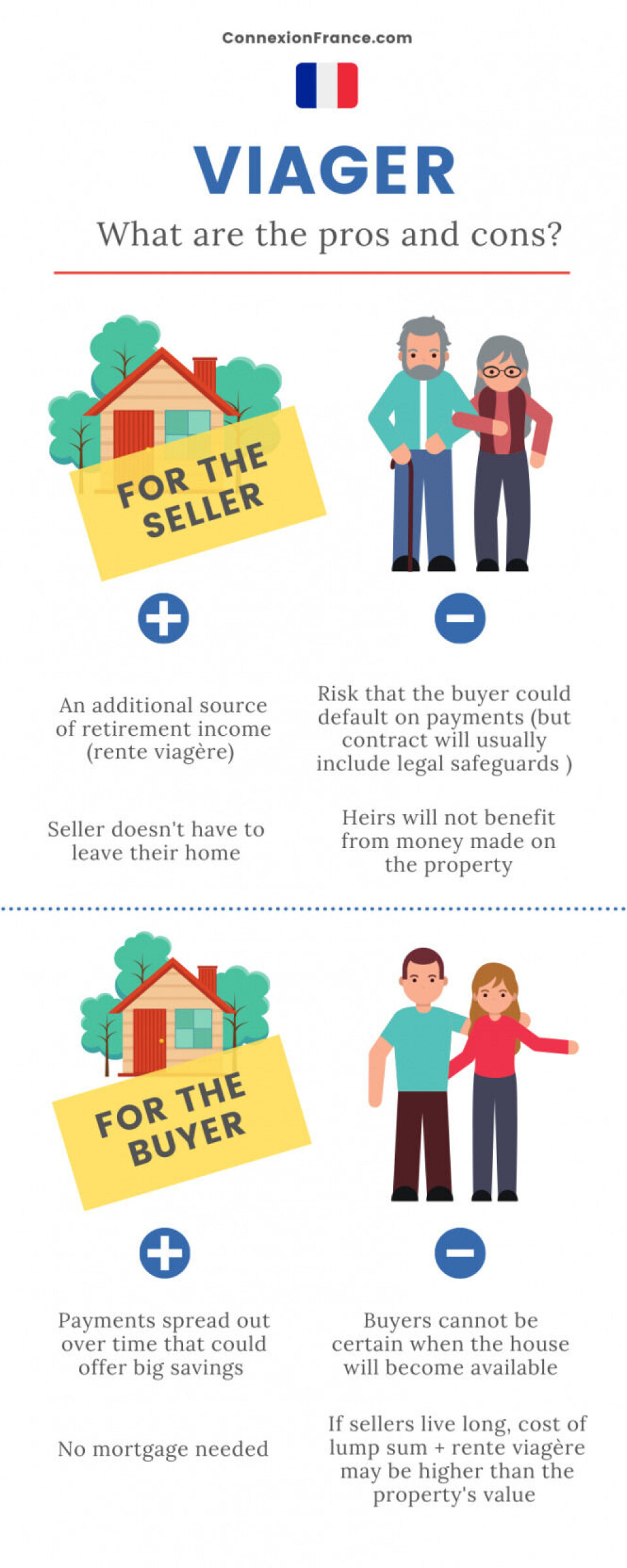

Buying and selling a home in France: What is the viager system?

France has an unusual way of buying and selling a home based on estimates of the seller’s life expectancy. In many cases it is the only realistic way for homeowners to release equity from their property

En viager in English means ‘for the lifetime.’ This type of home sale in France can offer the chance of a good deal for buyers and security for the seller.

It is also the only realistic way for an older homeowner with a modest income to ‘release equity’ from their property.

Meanwhile, the alternative crédit hypothécaire loan is secured against a property with its amount depending on ability to repay, rather than its value, and is repayable in the borrower's lifetime.

As such, “this old institution retains its usefulness in certain cases and the British are often especially curious about it,” said English-speaking notaire François Trémosa of Trémosa - Leschelle & Associés in Haute-Garonne.

What is the viager occupé?

In its most classic format, viager occupé, a viager sale involves the buyer paying part of the market value of the property to the seller as an upfront lump sum called the bouquet, often around 30% of the value.

The seller then maintains a lifetime right to use or live in the property whilst the buyer pays them a regular lifetime rent – rente viagère – on a monthly or three-monthly basis.

It can be a gamble for the two parties as the seller could live longer than average, meaning the buyer ends up paying more than anticipated. However, the seller might die earlier than expected, meaning a bargain for the buyer.

In this case, the seller will not have benefited for long and their heirs will have lost the chance to inherit the property.

Generally speaking, however, the notorious example of the world’s oldest woman Jeanne Calment, who outlived her viager buyer living to a ripe old age of 122, is a very rare event.

Sellers are often widows or widowers, or older couples, where the sale is called un viager sur deux têtes (viager ‘on two heads’). The sellers can also be any two or more people who own a property jointly.

How does viager work in France?

The future death of the seller, known as the crédirentier, must be unpredictable, so the buyer should not have inside knowledge of some serious illness the seller is suffering from, for example.

If the seller dies within 20 days of the sale, their heirs can ask a court to annul the sale.

What is the difference between viager libre and viageroccupé?

A viager can be libre (free) or occupé (occupied) – the former is less usual and means the property is sold unoccupied. The buyer can use it straight away, though they continue to pay a lifetime rent to the seller.

In the occupé version, the seller remains in the home with a lifetime usage until their death (or until the death of the second partner if the viager is sur deux têtes).

This right to lifetime usage is often a simple droit d’usage et d’habitation, with only the seller and close family being able to use the property.

Alternatively it may be a usufruit – a legal right to full lifetime use – where the seller may also rent out the property to someone else. Here, the rent paid to the seller by the buyer will be reduced.

At the time of the sale the buyer obtains the residual ownership of the property (minus the lifetime use rights), called nue-propriété.

What happens in the case of one of the joint owners dying?

After the death of the first member of a couple, the rent may continue to be paid exactly the same to the survivor.

In this case, the rent is réversible. In some cases there may be a clause saying it will be reduced proportionally – the rent is réductible.

Selling en viager

Selling in this way can be of interest to older people looking to stay in their own homes. As there will be no property to pass on, it may especially interest those without heirs.

It can also mean that children avoid having to contribute to fees for a retirement home under the French rules on responsibilities towards parents (obligation alimentaire).

Occasionally older people opt to sell their home en viager within their own family, which can create family tensions and legal complications around inheritance rights.

In these cases, notaires can decide not to accept the sale, but if they do, it is vital that everything is done according to valid market prices so the tax office can not accuse the seller of making a ‘disguised gift’ to avoid inheritance tax.

Related article: Six ways to reduce your French inheritance tax

Should I go through an estate agency or use a notaire?

Selling en viager can be done via an estate agency – some are specialised in the viager process, others arrange viagers as well as ordinary sales – or directly via certain notaires’ offices.

In all cases, the final sale contract containing the details of the arrangements will be drawn up by a notaire as an acte authentique (formal legal deed).

To find an agent or notaire, enquire at local agencies or search online with a term such as expert en viager or viagériste.

If you would like to find an English-speaking notaire in your area, visit the directory at notaires.fr and search by commune and then narrow the search by language spoken.

The sale contract will include certain clauses to protect the seller, such as a clause résolutoire, which states that the seller regains ownership of the property if several rental payments are missed.

Note however that, apart from the above situation, the sale is definitive. Sellers cannot bequeath the home to someone in their will and cannot sell it on to someone else.

Buying en viager

French viager investors tend to be in their late 40s and early 50s wanting to set themselves up with a retirement home for later life and hopefully get a good deal.

The total cost to the buyer to acquire the property is often effectively halved compared to the market price, in return for them accepting not having use of it for a number of years. Another plus is that, contrary to a mortgage, you do not pay any interest payments.

A viager purchase allows you to spread out the purchase of a property, similar to taking out a mortgage, but, as you are paying a member of the public and not a bank, there are no extra charges. There are however certain notaire fees payable by the buyer.

As with sellers, if you want to investigate a viager purchase, talk to local estate agents, viager specialists, or directly to notaires.

The notaires’ national property website shows a current selection of properties by clicking on consulter les annonces immobilières de vente en viager.

In the unlikely event of the buyer dying before the seller, the buyer’s heirs will have to continue paying the rent.

It is possible for the buyer to sell on the property at any time.

Viager costs for the buyer

Most viager sales involve a bouquet upfront, typically at 30% of the agreed market value of the home. However, the size of the bouquet is negotiable.

It is also possible to have an arrangement with a large bouquet but no rent, or no bouquet and more rent.

Finally, there is a viagerà terme, where the rent is payable only for a set number of years. The buyer still has to wait for the seller to die to recuperate the property.

How is the rent for en viager worked out?

The amount of the rent is also negotiable, but the agent or notaire will indicate what is reasonable, based on a calculation involving elements including:

- value of the propery

- amount of the bouquet

- estimated life expectancy of the seller

- rent that the seller could hope to obtain from it if they chose to rent it out

As these values involve estimates they are not set in stone. However, there are certain reference scales (barêmes) that are often used by notaires and agencies.

The ‘Barême Daubry’ is referred to as the référence (standard model) by French economics magazine Capital, and the publisher of the scale claims it is used by 50% of notaires’ offices.

Here is an example of the working out provided by the current edition of the Barême Daubry for a couple consisting of a man aged 73 and a woman aged 71:

The couple has a combined average life expectancy of 22 years

The value of the nue-propriété residual ownership that the buyer obtains in the sale is 41.7% of the full market value of the property, and the value of a droit d’usage et d’habitation retained by the couple is the remaining 58.3%

If the property is worth €200,000 and a bouquet (upfront lump sum) of €50,000 is paid over by the buyer, then the following calculation is made: Value of nue-propriété (ie. property rights obtained by seller factoring in possible occupation of the property for 22 years): €200,000 x 41.7% = €83,400

€83,400 minus €50,000 already paid = €33,400

Rent payable = €33,400 x 5.5% (a percentage rate meant to give a fair rent over the expected period) = €1,837/year, or 153/month.

Total rent paid during estimated 22 year period = €1,837 x 22 = €40,414.

What this means in practice

Once you add up the bouquet amount and total rent paid over 22 years this shows that if the couple has the expected average lifespan then the buyer will eventually obtain the property originally valued at €200,000 for a total of €90,414, though they have had to wait 22 years for it.

Note that also by this point it is likely its actual market value will have gone up.

In reality, the total cost to the buyer is however likely to be somewhat more than the figure given as there is often a clause d’indexation in the sale contract which states that the rent will be regularly revised upwards, using a cost of living index from national statistics body Insee, or average rises in French rents.

French income tax and other considerations

The rente viagère should be declared for income tax by the seller and is taxable at a percentage of its amount depending on the age of the seller at the time the first payment is made: 70% if aged under 50, 50% for 50-59, 40% for 60-69, and 30% for over 69.

There is no tax on the bouquet.

Other responsibilities depend on the type of viager, and should be clarified in the sale contract, such as:

Viager occupé with usufruit – the seller pays for the upkeep of the home, property taxes and utility bills, however major repairs (and works voted for by a building’s joint owners in the case of a flat) should be paid by the buyer.

Viager occupé with droit d’usage – If not specified otherwise in the contract, the buyer should pay the taxe foncière and tax for rubbish removal (otherwise, as above)

Viager libre – everything is paid for by the buyer.

A new option – viager mutualisé

The classic viager involves a contract between an individual seller and an individual buyer.

The viager mutualisé is a newer version in which an investment fund buys several properties en viager to spread the risk. Investors can invest in the funds, with their money typically held in the form of assurance-vie.

Read more:What is the Viager mutualisé?

One particular viager mutualisé is called Certivia, run in partnership with the notaires and certain major institutional partners, such as Crédit Mutuel, BNP Paribas and state bank Caisse des Dépôts.

Viager: Useful vocabulary to know

Crédirentier = the buyer, who owes a rent-for-life to the seller

Débirentier = the seller, to whom a lifetime rent is owned by the buyer

Bouquet = upfront lump sum paid to the seller

Rente viagère = lifetime rent paid to the seller

Une tête / deux têtes = in viager jargon, refers to one or two sellers

Usufruit = Right to live in property for life or rent it out to someone else

Droit d’usage et d’habitation = Right for yourself and close family to live in the home