-

Points to check before buying a property in France

Cracks, termites, electrical checks…what to look out for

-

Many Société Générale customers to be charged additional fees from April

There is some good news for international banking and instant transfers, however

-

When must a bank reimburse a customer scam victim in France?

Reimbursement can depend on whether the customer has been ‘negligent’

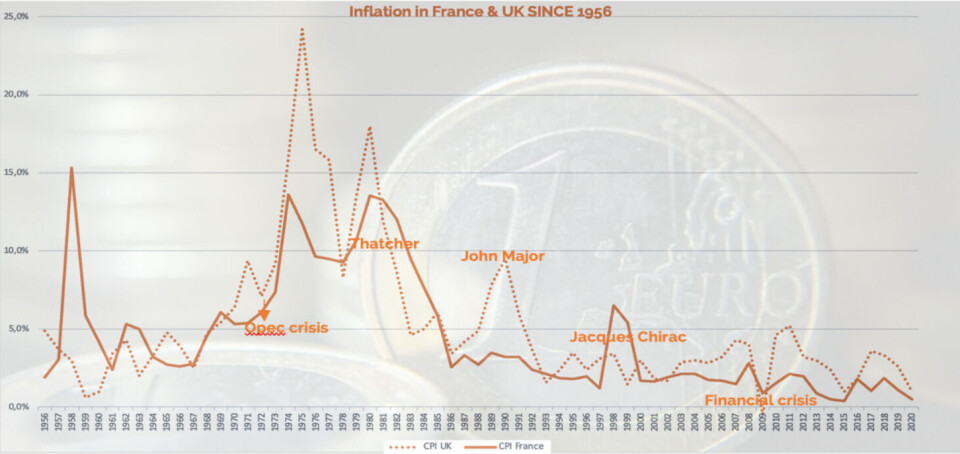

An inflationary tale: is inflation on the rise again?

Sponsored content: Investment insight by Andrew Hodson, Head of Investment Services at Strabens Hall

Markets continued to rise in the first quarter of 2021, emboldened by record amounts of fiscal stimulus, successful vaccine rollouts and strengthening economic data. Whilst this offers plenty to be optimistic about, increased inflationary pressures has introduced some uncertainty.

The most visible casualty has been the bond market where US Treasuries recorded their biggest losses since 1980 as yields rose sharply from their previous depressed levels. Though they remain historically low, a rapid rise in yields can ripple through to other assets, affecting everything from financial stocks to the housing market.

For the time being, central banks are allowing bond yields to rise to reflect an improving economic outlook and are likely to let inflation rise for a period. Interest rates, however, are expected to remain close to zero for at least two years.

Within equity markets, while a number of headline indices have reached record highs, this masks a substantial underlying rotation in leadership since the beginning of the year out of high ‘growth’ stocks, such as the large US technology companies into ‘value’ stocks; sectors more geared to a strong economic upturn, such as banking, oil and mining shares.

Over the last 15 years, as global growth has slowed and inflation has fallen, investors searching for returns have focused on growth stocks with their higher long-term earnings and defensive qualities. Covid and the move to working from home during lockdown accelerated the returns of these already fast growing technology companies such as e commerce, online payments and cloud software.

Value stocks, however, whilst more sensitive to economic cycles, have tended to underperform, and were punished further by the events of 2020 when they fell sharply in response to the sudden economic contraction triggered by lockdown. However, as we awake from lockdown we are now seeing a rotation from growth to value.

Advertisement

Why has inflation been low in recent years?

There are a number of factors behind the historically low levels of inflation seen over the last decade or so. These include a period of austerity following the 2008 financial crisis, increased competition through greater globalisation and investment in technology, providing a favourable environment for bonds and equities.

Should we be wary of exuberant spending plans?

There appears to be an appetite to unleash unprecedented amounts of monetary and fiscal stimulus to support economies and generate full employment with a notable shift in emphasis on climate change and inequality to ensure social stability.

In the short term there is evidence of inflationary pressures given the quantum of the stimulus. However, the question is, will a rise in inflation be short lived, fuelled by a post-lockdown surge as economies begin to reopen creating supply-side constraints, or can we expect an extended period of inflation given the greater political dimension and social and climate change agendas.

Time will tell, but for there to be sustained upward pressure on prices we would need to see sustained wage inflation, which is unlikely for some time given the current levels of unemployment and spare capacity following the pandemic. In the meantime, there are of course risks of an uneven recovery, as other parts of the developed and emerging world lag behind in their vaccination programmes, and virus mutations remain.

How do you protect your portfolio against inflation?

With the expectation that interest rates will remain low, inflationary pressures will hit cash accounts hardest, devaluing their spending power. Whilst it’s important to hold some cash, it should be seen as part of your overall investment strategy alongside a diversified and dynamic portfolio of investments.

It starts here

If you would like to find out more about our investment services, contact us at: startherefrance@strabenshall.eu

Strabens Hall France

37-41 Boulevard Dubouchage

06000 Nice

Strabens Hall UK

D'Arblay House

16 D'Arblay Street

London W1F 8EA

This communication is not intended to constitute and should not be construed as investment advice or investment recommendations or investment research